What is C/O Form EUR.1? Regulations and Declaration Guide

In Vietnam’s export activities to the European Union (EU), C/O Form EUR.1 is an important certificate of origin that allows Vietnamese exporters to enjoy preferential tariff treatment under the EVFTA agreement. However, many businesses in Vietnam still do not fully understand what C/O Form EUR.1 is, the conditions for issuance, and how to properly use it to avoid rejection of tariff preferences by EU customs authorities.

This article provides an overview of the definition, role, legal basis, and key regulations related to C/O Form EUR.1 for exporters in Vietnam under the latest EVFTA regulations.

1. What is C/O Form EUR.1?

1.1 Definition of C/O Form EUR.1

C/O Form EUR.1 (Certificate of Origin Form EUR.1) is a Certificate of Origin used in trade between Vietnam and the European Union (EU) under the framework of the EU-Vietnam Free Trade Agreement (EVFTA). This document is issued by a competent authority to certify that goods satisfy origin criteria and are eligible for preferential tariff treatment when exported to the EU market.

In essence, C/O Form EUR.1 acts as a “commercial passport” for exported goods — proving Vietnamese origin so that EU customs authorities can apply EVFTA preferential tariffs instead of the normal MFN (Most Favoured Nation) tariff rates.

C/O Form EUR.1 applies to goods exported from Vietnam to all 27 EU member states, including Germany, France, the Netherlands, Belgium, Italy, Spain, Poland, Sweden, Denmark, Finland, and other EU countries.

⚠️ Note:

Following Brexit (01/01/2021), the United Kingdom is no longer an EU member state. Goods exported from Vietnam to the UK must use C/O Form UKVFTA under the UK-Vietnam Free Trade Agreement, instead of C/O Form EUR.1.

Download the C/O Form EUR.1 Sample Here

1.2 How is C/O Form EUR.1 Different from Ordinary C/O?

Unlike ordinary certificates of origin used mainly for trade statistics purposes, C/O Form EUR.1 is a preferential certificate of origin directly linked to tariff benefits. Without a valid C/O Form EUR.1, Vietnamese exports entering the EU may be subject to normal import duties, which can be significantly higher than EVFTA preferential tariff rates.

1.3 The Role and Importance of C/O Form EUR.1

In modern international trade, certificates of origin play a crucial role. Specifically, the importance of C/O Form EUR.1 can be seen in the following aspects:

- Enjoying EVFTA tariff preferences: EVFTA commits the EU to eliminating or significantly reducing import duties on Vietnamese goods — many products benefit from tariff reductions from 10–20% MFN rates down to 0%. To receive these preferences, goods must have a valid C/O Form EUR.1 or a self-certification of origin where applicable.

- Enhancing competitiveness in the EU market: Lower tariff rates allow Vietnamese exporters to compete more effectively on price against suppliers from countries without FTAs with the EU.

- Reducing legal and customs risks: C/O Form EUR.1 serves as legal proof of origin, helping businesses avoid risks such as anti-fraud investigations, tax reassessment, or cargo seizure at EU ports.

- Expanding export opportunities: Many EU buyers only work with suppliers capable of providing complete origin documentation, in which C/O Form EUR.1 is often a mandatory requirement.

⚠️ Important:

According to Vietnam’s Ministry of Industry and Trade, exports to the EU have grown strongly since EVFTA came into effect in August 2020. The utilization rate of preferential tariffs through C/O Form EUR.1 has continuously increased, especially in textile, footwear, seafood, and electronics industries.

1.4 Legal Basis and Scope of Application

C/O Form EUR.1 is governed by the following legal documents:

| Legal Document | Relevant Content |

|---|---|

| EVFTA Agreement (Effective from 01 August 2020) | Tariff preference commitments and Protocol on Rules of Origin |

| Circular 11/2020/TT-BCT | Rules of origin under EVFTA and C/O sample forms |

| Decree 31/2018/ND-CP | Guidelines on origin of goods under Vietnam’s Foreign Trade Management Law |

| Circular 05/2018/TT-BCT | Regulations on authorized C/O issuing authorities |

| EU Implementing Regulation 2015/2447 | EU customs procedures related to origin verification |

2. Conditions for Obtaining C/O Form EUR.1

To obtain C/O Form EUR.1, both the goods and the exporter must satisfy the following conditions:

2.1 Conditions Related to Goods

- Compliance with origin rules: Goods must satisfy EVFTA origin criteria — either wholly obtained or sufficiently processed in Vietnam.

- Direct transportation requirement: Goods must be transported directly from Vietnam to the EU. If transshipment through a third country occurs, supporting evidence must prove that the goods were not further processed there.

- Eligible products: The products must fall within the scope of EVFTA tariff preference commitments.

2.2 Conditions Related to Exporters

- The exporter must register trader information with the competent C/O issuing authority.

- The company must maintain sufficient documents proving the origin of materials and manufacturing processes.

- The exporter must not be suspended from C/O issuance.

- The exporter must comply with origin declaration regulations and have no history of origin fraud violations.

2.3 Timing for Application Submission

Normally, applications for C/O Form EUR.1 should be submitted before or at the time of exportation. In special cases, retrospective issuance may be permitted for justified reasons, subject to approval by the issuing authority.

3. Rules of Origin Applicable to C/O Form EUR.1

This is the most technical and important part businesses need to understand. Under the EVFTA Protocol on Rules of Origin, there are three main criteria for determining Vietnamese origin:

Wholly Obtained Goods

Goods entirely produced, cultivated, harvested, or extracted in Vietnam without using imported materials. Examples include seafood caught in Vietnamese waters, agricultural products grown in Vietnam, and minerals extracted in Vietnam.

Sufficient Processing or Working

Goods may use imported materials but must undergo substantial transformation in Vietnam. This criterion may be assessed through:

(a) Change in Tariff Classification (CTC);

(b) Regional Value Content (RVC);

(c) Specific Processing Operations.

Cumulation of Origin

EVFTA allows bilateral cumulation, meaning materials originating in the EU and used in production in Vietnam may be treated as Vietnamese-origin materials. This creates additional opportunities for industries such as textiles and electronics.

Regional Value Content (RVC)

RVC calculation formula under EVFTA:

RVC (%) = (FOB Value – Value of Non-Originating Materials) / FOB Value × 100%

Typically, the minimum RVC requirement is 40% under the build-down method or 30% under the build-up method, depending on the specific product.

Each product category has different Product Specific Rules (PSR). Businesses should refer to Appendix II of Circular 11/2020/TT-BCT based on the HS code of the goods to determine the correct applicable origin criterion.

4. Application Dossier and Procedures for C/O Form EUR.1

4.1 Authorities Authorized to Issue C/O Form EUR.1 in Vietnam

In Vietnam, C/O Form EUR.1 is issued by the Ministry of Industry and Trade (MOIT) through authorized organizations, including Regional Import-Export Management Offices (in Hanoi, Ho Chi Minh City, and other provinces), as well as several authorized Industrial Zone and Economic Zone Management Boards.

Businesses can now submit applications for C/O Form EUR.1 online through the Ministry of Industry and Trade’s electronic system at

ecosys.gov.vn.

4.2 Required Application Documents

- Application Form for C/O Form EUR.1: Completed according to the prescribed format, including full information about the goods, shipment, exporter, and importer.

- Completed C/O Form EUR.1: One original copy (official blank form) and one duplicate copy for record keeping.

- Export Customs Declaration: A certified copy or a printout from the VNACCS/VCIS customs system.

- Commercial Invoice: A copy clearly showing product value, goods description, seller, and buyer information.

- Bill of Lading / Airway Bill: A copy proving the actual transportation of goods.

- Declaration of Origin: A self-declared document explaining the production process and origin of materials.

- Raw Material Purchase Invoices / Import Declarations: Documents proving the origin of input materials.

- Bill of Materials (BOM): Required for processed or manufactured goods using imported materials.

4.3 Processing Time and Issuance Fees

| Application Type | Processing Time | Issuance Fee |

|---|---|---|

| Normal Application | Up to 3 working days after receiving complete and valid documents | According to current Ministry of Finance regulations |

| Urgent Application | Within the same working day or up to 8 working hours | Additional urgent processing fee may apply depending on local regulations |

| Retrospective Issuance | Subject to explanation and approval | Equivalent to normal issuance fees |

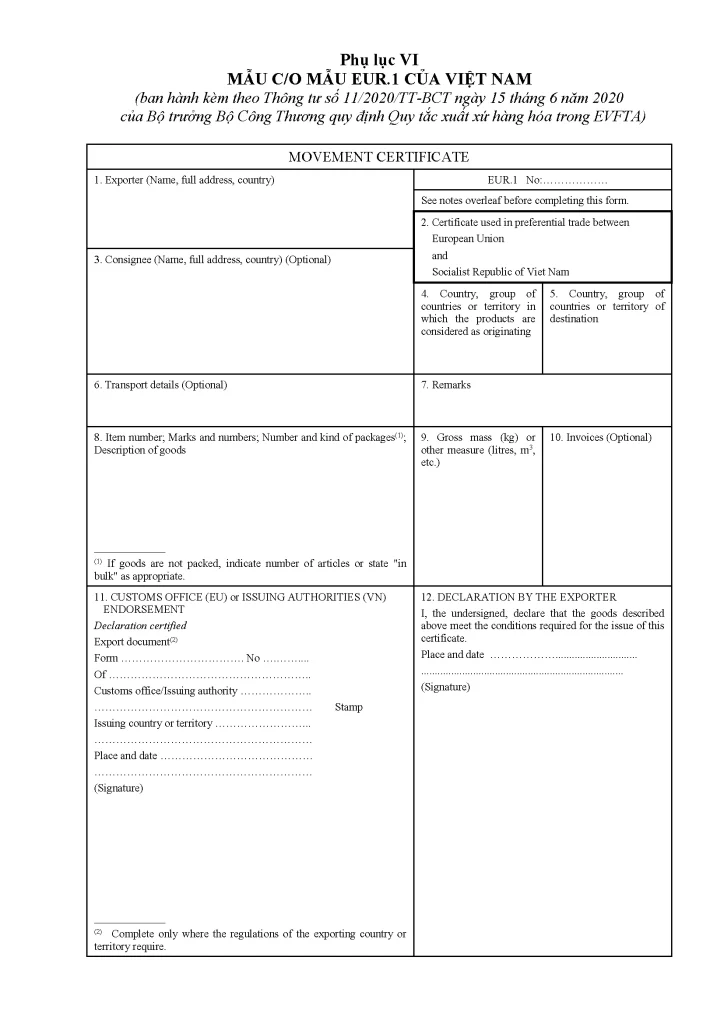

5. How to Complete Each Box on C/O Form EUR.1

| Box No. | Content | Completion Instructions |

|---|---|---|

| 01 | Exporter | Enter the full company name, registered address, and country (Vietnam). The information must match the Commercial Invoice and trader registration records. Do not abbreviate the company name. |

| 02 | Application for a Movement Certificate | Tick the appropriate box. Normally select “EUR.1” for standard applications. Select “EUR-MED” if Pan-Euro-Med cumulation applies. |

| 03 | Consignee | Enter the full name and address of the buyer/importer in the EU. The information must match the Commercial Invoice. If “To Order” is used, it must comply with the Bill of Lading requirements. |

| 04 | Country of Exportation | Enter: VIETNAM (uppercase, in English). Do not use “VN” or incorrect formats. |

| 05 | Country of Destination | Enter the importing EU country such as GERMANY, FRANCE, NETHERLANDS, etc. “EU” may be used if the final destination country is not yet determined. |

| 06 | Transport Details | Specify the mode of transport and shipment details: By sea / By air / By road, vessel or flight name, port of loading and port of discharge. Example: By sea, vessel MV EVER GIVEN, Ho Chi Minh Port to Hamburg Port. |

| 07 | Remarks | Include additional information if applicable, such as contract number, L/C number, or special buyer requirements. This box may be left blank if unnecessary. |

| 08 | Marks and Numbers; Description of Goods | Enter package marks, product description in English, HS code (6 digits), quantity, and unit of measurement. The description must be sufficiently detailed and consistent with the Commercial Invoice. |

| 09 | Gross Mass or Other Measure | Enter the gross weight in kilograms or other appropriate measurement units such as liters, m², or pieces. The information must match the Packing List. |

| 10 | Invoices | Enter the Commercial Invoice number and issuance date. If multiple invoices are involved, list all of them for reference. |

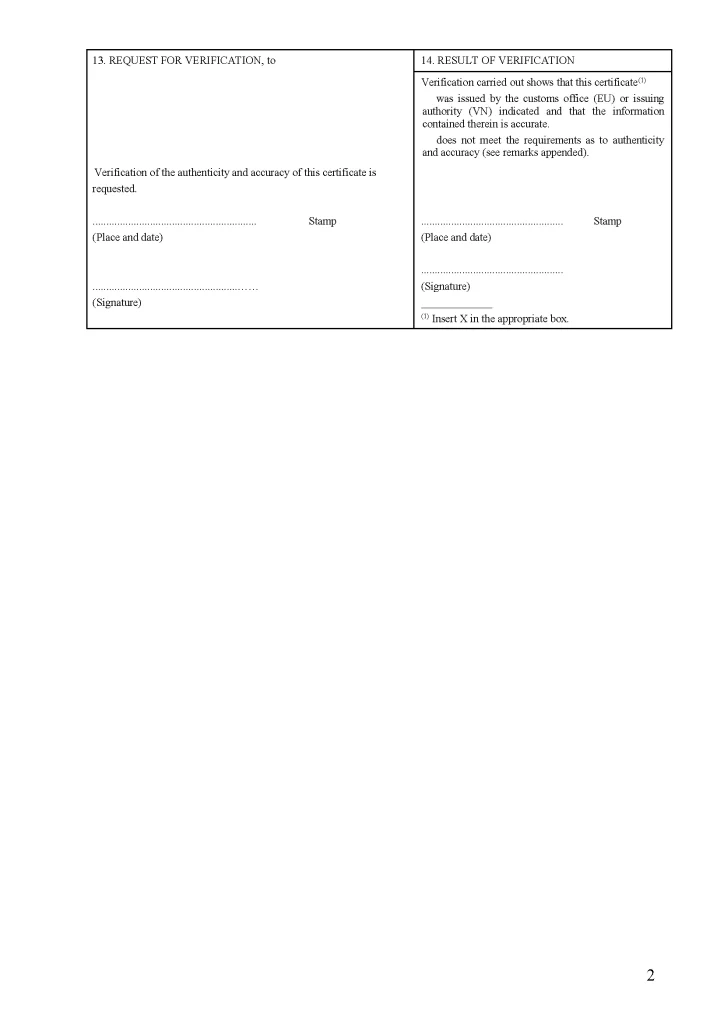

| 11 | Customs Endorsement | This box is reserved for confirmation and stamping by Vietnamese Customs authorities. The exporter must not complete this section. |

| 12 | Declaration by the Exporter | The exporter or authorized representative must sign, indicate the place and date of declaration, and affix the company stamp. The signature must match the registered specimen signature. |

Declaration LanguageC/O Form EUR.1 is pre-printed in both English and French. Exporters should complete the form in English. Correction fluid or erasures are not allowed; any errors require cancellation and reissuance of the form. Permanent ink, preferably black ink, should be used.

6. Comparison Between C/O Form EUR.1 and Other Common C/O Forms

| Criteria | C/O Form EUR.1 (EVFTA) | C/O Form D (ASEAN) | C/O Form A (GSP) | C/O Form AI (AIFTA) |

|---|---|---|---|---|

| Applicable Agreement | EVFTA | ATIGA | GSP Scheme | AIFTA |

| Target Market | 27 EU countries | ASEAN member states | GSP granting countries | India |

| Issuing Authority | Ministry of Industry and Trade | Ministry of Industry and Trade | MOIT / VCCI | Ministry of Industry and Trade |

| Validity Period | 10 months | 12 months | 10 months | 12 months |

| Minimum RVC Requirement | 40% (build-down) | 40% | Depends on importing country | 35% |

| Self-Certification | Yes (REX, shipments over 6,000 EUR) | Under implementation | No | No |

Exporters to the EU should note that C/O Form EUR.1 is the primary certificate accepted by EU customs authorities for EVFTA tariff preferences (unless origin is self-certified under the REX system). Other forms such as Form D or Form A do not qualify for EVFTA preferential treatment in the EU.

Other C/O forms such as Form D and Form A are not eligible for EVFTA preferential tariff treatment in the EU.

Explore other C/O forms:

7. FAQ – C/O Form EUR.1

Under EVFTA garment origin rules, besides fabric originating from the EU and South Korea, can fabric be imported from other countries for obtaining C/O Form EUR.1?

For garments exported under EVFTA using C/O Form EUR.1, the agreement currently allows extended cumulation only for fabrics originating from EVFTA member countries and South Korea. Fabrics imported from other countries outside these regions are not eligible for cumulation.

This rule is specified in Circular No. 11/2020/TT-BCT dated 15 June 2020 issued by the Ministry of Industry and Trade regarding Rules of Origin under EVFTA.

For exports to the EU, should companies use a REX number or C/O Form EUR.1?

Currently, exports to the EU under EVFTA may still use the traditional green paper C/O Form EUR.1 or self-certification of origin if the exporter satisfies the required conditions. The REX number mainly applies to the EU’s self-certification mechanism and certain preferential programs; it is not mandatory for all exports to the EU.

If Box No. 3 (Consignee) shows a UK company while the importing country is the Netherlands, can a C/O Form EUR.1 still be issued?

Yes. The consignee in Box No. 3 is not required to be an EU-based company. As long as transport documents such as the Bill of Lading and customs declaration show that the goods are actually imported into an EVFTA member country (for example, the Netherlands), C/O Form EUR.1 can still be issued normally.

Hello, I’m Nguyen Phuong Nhan (Ms. Nina)

I currently serve as Trade Lanes Supervisor at 3W Logistics, with more than 10 years of experience in international logistics and freight forwarding.

My primary responsibility is developing and managing global logistics partnerships, building strategic trade lanes, and working closely with overseas agents to provide reliable and competitive transportation solutions for customers.

I regularly collaborate with agents and logistics partners worldwide to explore new business opportunities, negotiate freight rates, develop trade routes, and support import-export shipments. I also work closely with our sales team to design logistics solutions tailored to specific markets and customer requirements.

My expertise includes Ocean Freight, Air Freight, Trade Lane Development, Global Agent Network Management, International Logistics Solutions, and Import-Export Support.

Through the articles I share on the 3W Logistics website, I aim to provide practical insights into the international logistics industry, global transportation trends, overseas agent cooperation, and effective logistics strategies that help businesses optimize their supply chain operations.

I believe that strong global partnerships and well-developed trade lanes are essential to delivering sustainable logistics solutions and long-term value to customers worldwide.