EUR 1 UK Certificate: Full Guide for Vietnamese Exporters

The EUR 1 UK certificate is the mandatory proof of origin for Vietnamese goods exported to the United Kingdom under the UK–Vietnam Free Trade Agreement (UKVFTA), granting preferential tariff rates instead of the standard MFN duty. Since UKVFTA entered into force on 1 May 2021, this certificate has become the key document for exporters competing on price in the UK market.

This guide covers everything your import-export team needs to act independently: the definition and legal basis of the EUR 1 UK, origin criteria, required documents, the step-by-step eCOSys filing process, box-by-box declaration instructions, the most common errors — and answers to six frequently asked questions.

1. What Is the EUR 1 UK Certificate?

The EUR 1 UK certificate — formally known as the Movement Certificate EUR.1 issued under the UKVFTA framework — is an official document confirming that goods satisfy the rules of origin set out in the UK–Vietnam Free Trade Agreement. UK customs authorities accept the EUR 1 UK to apply the preferential duty rates committed under UKVFTA instead of the default MFN tariff.

The EUR 1 form originated within the EU’s certification system. After Brexit, the United Kingdom and Vietnam concluded a separate bilateral agreement — UKVFTA — which retained the EUR 1 format under the designation EUR 1 UK (also written as EUK 1 UK in the eCOSys platform interface and some Ministry of Industry and Trade internal documents).

| Criterion | Details |

|---|---|

| Certificate name | EUR 1 UK (Movement Certificate EUR 1) |

| Applicable agreement | UKVFTA – UK–Vietnam Free Trade Agreement |

| UKVFTA entry into force | 1 May 2021 |

| Issuing authority in Vietnam | Regional Import-Export Management Division – Ministry of Industry and Trade |

| Filing system | eCOSys (ecosys.gov.vn) |

| Destination market | United Kingdom (Great Britain + Northern Ireland) |

| Certificate validity | 10 months from the date of issue |

Download the EUR 1 UK Certificate Template Here

See also: What is a Certificate of Origin (C/O)? , What is CO Form EAV?, What is CO Form VI?,…

2. EUR 1 UK vs Other Certificates of Origin

Many businesses confuse the EUR 1 UK with the EUR 1 certificate issued under EVFTA (for exports to EU member states) or with Form A under the UK Generalised Scheme of Preferences (UK GSP). These three instruments differ fundamentally in destination market, rules of origin, and the authority that verifies them.

| C/O Type | Agreement | Destination Market | Primary Origin Rule |

|---|---|---|---|

| EUR 1 UK | UKVFTA | United Kingdom | PSR per Annex II of UKVFTA |

| EUR 1 (EVFTA) | EVFTA | 27 EU member states | PSR per Annex II of EVFTA |

| Form A | UK GSP | United Kingdom | WO or SP under UK GSP Rules |

| Form B | UKVFTA (fallback) | United Kingdom | Same as EUR 1 UK, but self-certified by the exporter |

Note: From 1 January 2022, the UK GSP replaced the EU GSP for the UK market. If goods cannot satisfy the UKVFTA Product-Specific Rules (PSR), exporters may still consider Form A under the UK GSP — though preferential margins may be lower. Compare both options carefully before deciding.

3. Origin Criteria for the EUR 1 UK Certificate

Goods must meet one of three origin criteria prescribed in the UKVFTA implementing regulations issued by the Ministry of Industry and Trade. Identifying the correct criterion for each shipment before filing is essential — applying the wrong criterion is one of the top causes of C/O rejection at UK customs.

3.1 WO – Wholly Obtained

WO (Wholly Obtained) applies to goods produced entirely in Vietnam from materials of Vietnamese origin, with no imported inputs whatsoever. Typical product groups include agricultural produce, seafood caught in Vietnam’s exclusive economic zone, and minerals extracted domestically.

- Seafood caught within Vietnam’s exclusive economic zone

- Agricultural products grown and harvested in Vietnam

- Minerals extracted entirely within Vietnamese territory

- Goods manufactured solely from WO-qualifying materials

3.2 PSR – Product-Specific Rules

PSR (Product-Specific Rules) is the most commonly applied criterion for UKVFTA exports. Each HS code heading carries one or a combination of specific rules set out in Annex II of UKVFTA. PSR typically requires one of the following three conditions:

- CTC (Change in Tariff Classification) – Imported materials change their tariff heading after processing in Vietnam. CTC has three levels: CTH (chapter change), CTSH (6-digit subheading change), CTC (tariff item change).

- RVC (Regional Value Content) – The value added in Vietnam reaches the required threshold, generally 40–55% depending on the HS code. Calculated using either the Build-Down or Build-Up formula.

- SP (Specific Process) – A defined manufacturing process performed in Vietnam; applies primarily to textiles and chemicals.

Practical example: Exporting leather footwear (HS 6403) to the UK. The PSR requires CTH: upper and sole materials imported from China must change to HS heading 6403 after processing in Vietnam. If satisfied, the shipment qualifies for the EUR 1 UK and enjoys 0% duty instead of the ~8% MFN rate.

3.3 Cumulation

UKVFTA permits bilateral cumulation between Vietnam and the United Kingdom. Materials originating in the UK and used in Vietnamese manufacturing count as domestic inputs when calculating RVC or determining CTC compliance. This creates a significant advantage for businesses that import UK machinery or components for processing goods exported back to the UK.

4. Required Documents for the EUR 1 UK Certificate

All documents for the EUR 1 UK are submitted electronically through eCOSys. Prepare every item before starting the online declaration to avoid rejection or supplementary requests that could delay cargo cut-off.

- C/O Application Form (Ministry of Industry and Trade template, completed directly on eCOSys)

- Confirmed Export Customs Declaration (certified copy, post-clearance)

- Sales Contract with the UK buyer

- Commercial Invoice matching the export shipment

- Bill of Lading or Airway Bill (Through B/L if the goods transit a third country)

- Import Customs Declaration for Raw Materials (mandatory when imported inputs are used, to prove CTC or RVC compliance)

- RVC Calculation Sheet or CTC Analysis Table (depending on the applicable origin criterion)

- Manufacturing Declaration / Production Process Statement prepared by the exporter

- Domestic Raw Material Purchase Invoices (when applying WO or calculating RVC)

- Export Licence (if the goods fall under a conditionally controlled export category)

Note: For first-time shipments or new product lines, the issuing authority may require a physical factory inspection. Companies should register at least five working days in advance to avoid disrupting the shipping schedule.

5. Step-by-Step EUR 1 UK Filing on eCOSys

The entire EUR 1 UK application process is handled 100% online through ecosys.gov.vn. Standard processing time is 1–3 working days from the date a complete dossier is accepted.

- Log in to eCOSys at ecosys.gov.vn → Select “C/O Declaration” → Choose certificate type: EUR 1 UK (UKVFTA).

- Enter shipment details: Goods description, HS code, FOB value, contract number, Invoice number, B/L number, port of loading, port of destination (UK).

- Select origin criterion: Choose WO, CTC (CTH/CTSH), RVC, or SP matching the PSR for the relevant HS code. The system will prompt for the corresponding supporting documents.

- Upload electronic documents: Scan all documents listed in Section 4 in colour. Ensure PDFs are clearly legible and named according to system requirements.

- Review and submit: Verify all declared information. Click “Submit Dossier” — the system generates a reference number for tracking.

- Monitor processing: The Regional Import-Export Management Division reviews the dossier. If supplementary documents are needed, the system notifies the registered email. Respond within 24 hours to protect vessel schedule.

- Receive and stamp the C/O: Once approved, print the EUR 1 UK using the prescribed template and bring the printout with the original dossier to the Regional Import-Export Management Division for signature and stamp (unless the company holds Approved Exporter status for self-certification).

- Present to UK customs: Attach the original EUR 1 UK to the commercial documents sent to the UK buyer or freight forwarder for customs clearance and preferential duty application.

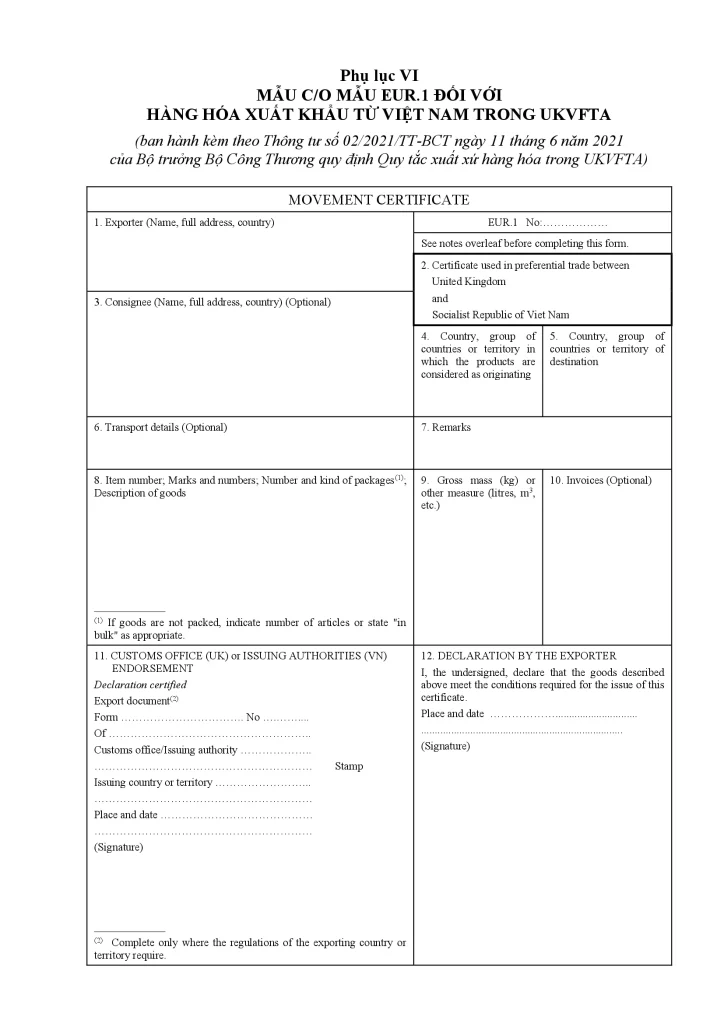

6. Box-by-Box Declaration Guide for the EUR 1 UK

The EUR 1 UK form contains 14 boxes. An error in any single box may result in rejection at UK customs or withdrawal of preferential treatment following a post-clearance audit.

| Box | Field Name | Declaration Guidance |

|---|---|---|

| 1 | Exporter | Full name and address of the Vietnamese exporter, exactly as on the contract and Invoice |

| 2 | Certificate No. | Assigned by the issuing authority — do not self-populate |

| 3 | Consignee | Full name and address of the UK consignee. “To Order” is acceptable for order B/Ls |

| 4 | Country of origin | Enter: Vietnam |

| 5 | Country of destination | Enter: United Kingdom |

| 6 | Transport details | Vessel/airline name, voyage/flight number, port of loading, port of discharge in the UK |

| 7 | Remarks | Contract number, Invoice number, or special notations (back-to-back C/O, exhibition goods, etc.) |

| 8 | Item number, marks, description | Sequential item number, package marks, and goods description copied verbatim from the Invoice — no abbreviations |

| 9 | HS Code | 6-digit HS code from the current Vietnamese tariff schedule |

| 10 | Gross weight / Quantity | Actual weight (kg) or quantity (pcs/cartons) matching the Packing List |

| 11 | Invoice value | FOB value in the currency stated on the Invoice — no self-conversion |

| 12 | Origin criterion | Enter the criterion code: WO, CTH, CTSH, RVC [X%], or SP |

| 13 | Declaration by exporter | Signature of authorised representative + declaration date + company name |

| 14 | Endorsement by competent authority | Regional Import-Export Management Division signature, stamp, and issue date |

Note: Box 12 (Origin criterion) is the most frequently mis-declared field. When applying RVC, state the percentage explicitly — for example: RVC 45%. When applying CTH, enter only CTH — no percentage is required. A blank or incorrect Box 12 is the single leading cause of EUR 1 UK rejection at UK ports of entry.

7. Common Declaration Errors and How to Fix Them

Analysis of EUR 1 UK certificates rejected at UK customs shows that the vast majority of errors stem from the documentation stage, not from the goods themselves. Early identification saves time and prevents loss of preferential tariff benefits across an entire consignment.

| Common Error | Consequence | Remedy |

|---|---|---|

| Box 8 goods description does not match the Invoice | UK customs suspects fraud; goods held pending investigation | Copy the goods description verbatim from the Commercial Invoice into Box 8 |

| Box 12 left blank or wrong criterion code entered | C/O deemed invalid; preferential tariff lost | Look up PSR for the HS code before filing; enter the correct code (WO / CTH / RVC X%) |

| Incorrect currency in Box 11 FOB value | Customs requires amendment; DEM/DET charges accumulate | Use the exact currency on the Invoice; no independent conversion |

| Dossier submitted more than 3 days after the export date | Must apply for a Retrospective C/O; additional procedural steps required | Submit on eCOSys immediately after the export customs declaration is confirmed |

| No import customs declaration attached for raw materials | Dossier returned; C/O issuance delayed | Prepare import declarations and raw material purchase invoices in advance |

| EUR 1 (EVFTA form) used for exports to the UK | UK customs rejects the entire shipment; no duty refund | Confirm destination market: UK → EUR 1 UK; EU → EUR 1 |

| HS code mismatch between the C/O and the export customs declaration | Documents deemed inconsistent | Use a single, consistent HS code across all shipment documents |

8. Can the EUR 1 UK Be Issued After Goods Have Shipped?

Yes. UKVFTA provides for a Retrospective C/O when a shipment has departed before the EUR 1 UK could be obtained — provided the delay is caused by a system technical failure or a verified force majeure event confirmed by the competent authority.

The application for retrospective issuance must be filed within 12 months of the export date, accompanied by a written explanation and evidence that the goods were actually exported. A retrospective EUR 1 UK carries an additional endorsement — “ISSUED RETROSPECTIVELY” — stamped in Box 7, and is accepted by UK customs when the dossier is complete.

9. Frequently Asked Questions About the EUR 1 UK Certificate

How long is the EUR 1 UK certificate valid?

The EUR 1 UK is valid for 10 months from the date the competent authority signs and stamps it. If goods arrive in the UK after the 10-month period, the certificate is no longer valid and the UK importer must pay the MFN rate. Always factor transit time into planning to ensure the certificate is still valid at the time of UK customs clearance.

Can goods transiting a third-country port use the EUR 1 UK?

Yes. Vietnamese goods transiting through Singapore, Port Klang, Hong Kong, or other hubs remain eligible for the EUR 1 UK provided the Direct Consignment rule is satisfied: the goods must not undergo any working or processing in the transit country, and transit country customs must be able to confirm the goods were only in transit. Additional documents required: a Through Bill of Lading from the Vietnamese port directly to the UK port, or a Transit Declaration issued at the transhipment port.

Can small businesses apply for the EUR 1 UK themselves?

Any company with a registered eCOSys account can self-file the EUR 1 UK application. However, to self-certify origin without submitting to an issuing authority — under the Approved Exporter mechanism — the company must be formally recognised by the Ministry of Industry and Trade following an assessment of its compliance capacity. Small businesses exporting to the UK for the first time are advised to obtain the certificate through the Regional Import-Export Management Division to minimise risk.

Can a returned shipment receive a new EUR 1 UK?

If a shipment is returned due to a commercial issue (not an origin deficiency), the exporter may apply for a new EUR 1 UK when the goods are re-exported. The original certificate cannot be reused because it will have expired or will no longer correspond to the actual shipment. If origin fraud is suspected, the Ministry of Industry and Trade will coordinate verification with UK customs before issuing a replacement certificate.

Is UKVFTA still in force? What are the current preferential tariff rates?

UKVFTA has been fully in force since 1 May 2021. Under the agreed schedule, the UK will eliminate approximately 99% of tariff lines on Vietnamese goods in phased reductions through to 2031. Key Vietnamese export categories — including seafood, garments, footwear, and wood products — already enjoy 0% or deeply reduced rates from the first year of implementation.

10. Conclusion: Four Steps to Use the EUR 1 UK Effectively

To export to the UK and maximise UKVFTA preferential tariffs through the EUR 1 UK, your team needs to complete four foundational steps:

- Verify the precise HS code and look up the corresponding PSR in Annex II of UKVFTA to determine the applicable origin criterion (WO, CTH, CTSH, RVC, or SP).

- Prepare a complete origin-proof dossier — especially import customs declarations for raw materials and the RVC/CTC calculation sheet — at least three working days before the export date.

- Declare all 14 boxes on the EUR 1 UK form accurately and completely, with particular attention to Box 8 (goods description) and Box 12 (origin criterion).

- Submit the electronic dossier on eCOSys immediately after the export customs declaration is confirmed; monitor processing status and respond to any supplementary requests promptly to receive the C/O before cargo cut-off.

This article is compiled based on the UKVFTA implementing circular issued by the Ministry of Industry and Trade, Decree No. 111/2020/NĐ-CP on preferential certificates of origin, and the technical guidelines of the eCOSys platform.

3W Logistics – Your EUR 1 UK Certificate Partner for UK Exports

Applying for the EUR 1 UK demands precise PSR lookup by HS code, multi-layer documentation, and tight coordination between procurement, accounting, and import-export teams — all within a very short window. A single error in Box 12 or a missing raw material import declaration can cost an entire shipment its UKVFTA preferential rate, exposing it to MFN duties of 8–20% depending on the product group. 3W Logistics works alongside hundreds of Vietnamese exporters to process C/Os accurately and on time.

- C/O & FTA specialist team: 3W Logistics specialists have deep knowledge of the PSR requirements under UKVFTA, EVFTA, CPTPP, RCEP, and other next-generation FTAs. We look up origin criteria precisely at the 8-digit HS level, prepare RVC calculation sheets, and compile complete declaration dossiers — so businesses avoid C/O rejection from the very first submission.

- Integrated logistics network – Global NVOCC: With NVOCC capability on the Vietnam–UK corridor (via Felixstowe, Southampton, and London Gateway), 3W Logistics controls the full transport chain from factory to destination port, guaranteeing valid Through B/Ls — the critical condition for a EUR 1 UK to withstand scrutiny under the Direct Consignment rule.

- Fast processing, minimised DEM/DET: The 3W Logistics customs team prepares the complete export document set (Invoice, Packing List, B/L, EUR 1 UK certificate) in parallel with the vessel schedule, ensuring the C/O is ready before cut-off — reducing the risk of container detention and DEM/DET charges at UK ports.

For enquiries about UKVFTA origin consulting, EUR 1 UK certificate support, or end-to-end freight services to the UK market, contact 3W Logistics today for a comprehensive solution.

CONTACT INFORMATION:

Head Office – 3W Logistics Ho Chi Minh City Branch

Address: 34 Bach Dang, Tan Son Hoa Ward, Ho Chi Minh City

Hotline: +84 28 3535 0087

3W Logistics Hanoi Branch

Address: 81A Tran Quoc Toan, Cua Nam Ward, Hanoi

Hotline: +84 24 3202 0482

3W Logistics Hai Phong Branch

Address: 8A Lot 28 Le Hong Phong, Gia Vien Ward, Hai Phong

Hotline: +84 225 355 5939

3W LOGISTICS CO., LTD – We here serve you there!

Email: quote@3w-logistics.com

Website: www.3w-logistics.com

Hello, I’m Nguyen Phuong Nhan (Ms. Nina)

I currently serve as Trade Lanes Supervisor at 3W Logistics, with more than 10 years of experience in international logistics and freight forwarding.

My primary responsibility is developing and managing global logistics partnerships, building strategic trade lanes, and working closely with overseas agents to provide reliable and competitive transportation solutions for customers.

I regularly collaborate with agents and logistics partners worldwide to explore new business opportunities, negotiate freight rates, develop trade routes, and support import-export shipments. I also work closely with our sales team to design logistics solutions tailored to specific markets and customer requirements.

My expertise includes Ocean Freight, Air Freight, Trade Lane Development, Global Agent Network Management, International Logistics Solutions, and Import-Export Support.

Through the articles I share on the 3W Logistics website, I aim to provide practical insights into the international logistics industry, global transportation trends, overseas agent cooperation, and effective logistics strategies that help businesses optimize their supply chain operations.

I believe that strong global partnerships and well-developed trade lanes are essential to delivering sustainable logistics solutions and long-term value to customers worldwide.