What is C/O Form D? How to declare it and the latest regulations today

C/O Form D is the most important certificate of origin used in intra-ASEAN trade, helping import-export businesses enjoy special preferential tariff rates — even 0% — under the ASEAN Trade in Goods Agreement (ATIGA).

If you are exporting goods to ASEAN countries such as Thailand, Indonesia, Malaysia, the Philippines, or Singapore, understanding and declaring C/O Form D correctly can not only reduce import duties significantly but also help avoid the risk of rejection by customs authorities in the importing country.

In this article, 3W Logistics provides a complete guide covering the definition, eligibility requirements, detailed box-by-box instructions, application procedures, and common mistakes businesses should avoid when using C/O Form D.

1. What is C/O Form D?

C/O Form D (Certificate of Origin Form D) is a certificate of origin issued for goods exported from one ASEAN member country to another ASEAN member country to certify that the goods meet the origin requirements under the ASEAN Trade in Goods Agreement (ATIGA).

Under Vietnamese regulations, C/O Form D is issued based on:

- Circular No. 19/2020/TT-BCT dated August 14, 2020, issued by the Ministry of Industry and Trade regarding rules of origin under ATIGA

- The ASEAN Trade in Goods Agreement (ATIGA), signed in 2009 and effective from 2010

- Appendix 8 of the ATIGA Agreement regulating procedures for issuance and verification of certificates of origin

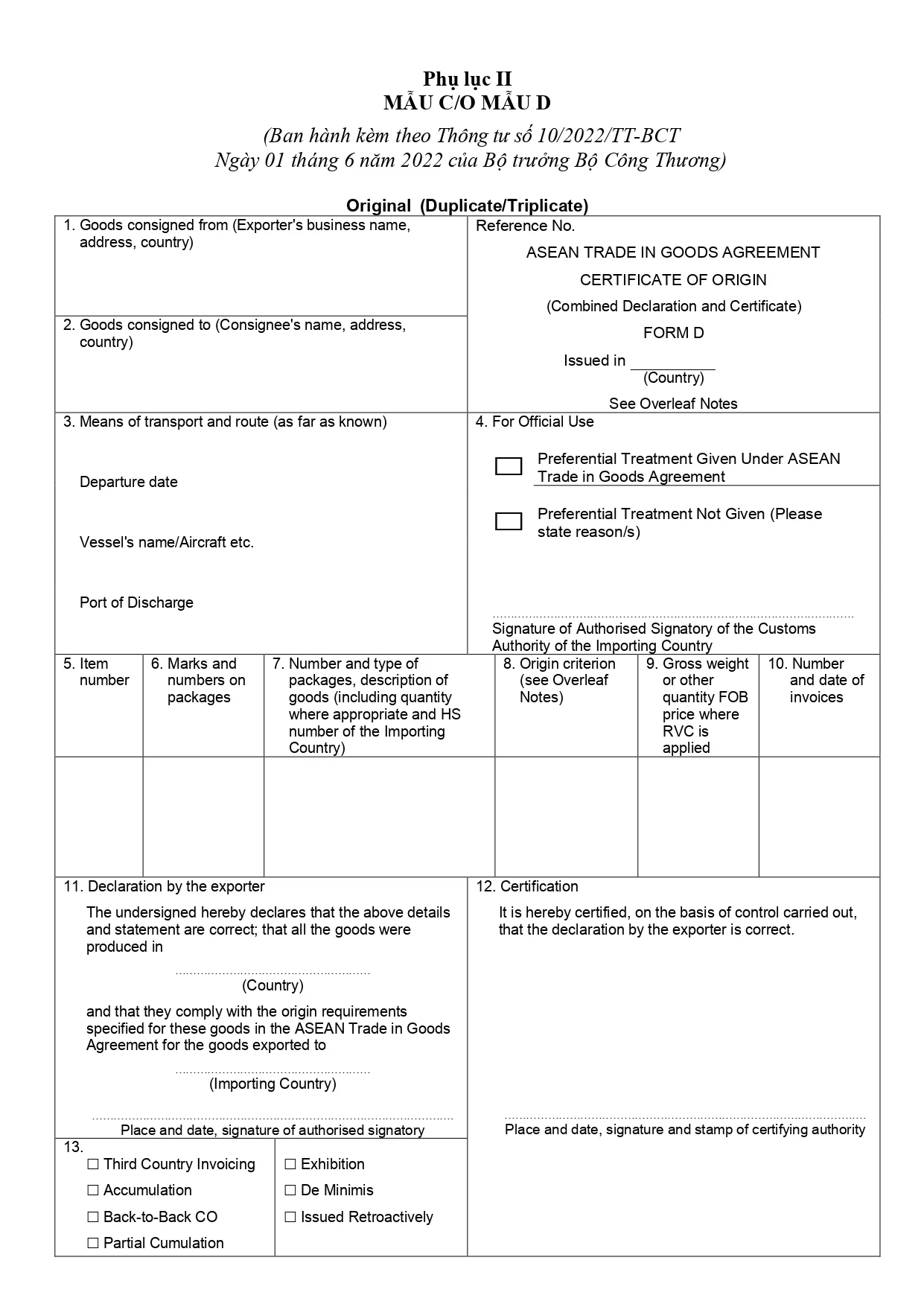

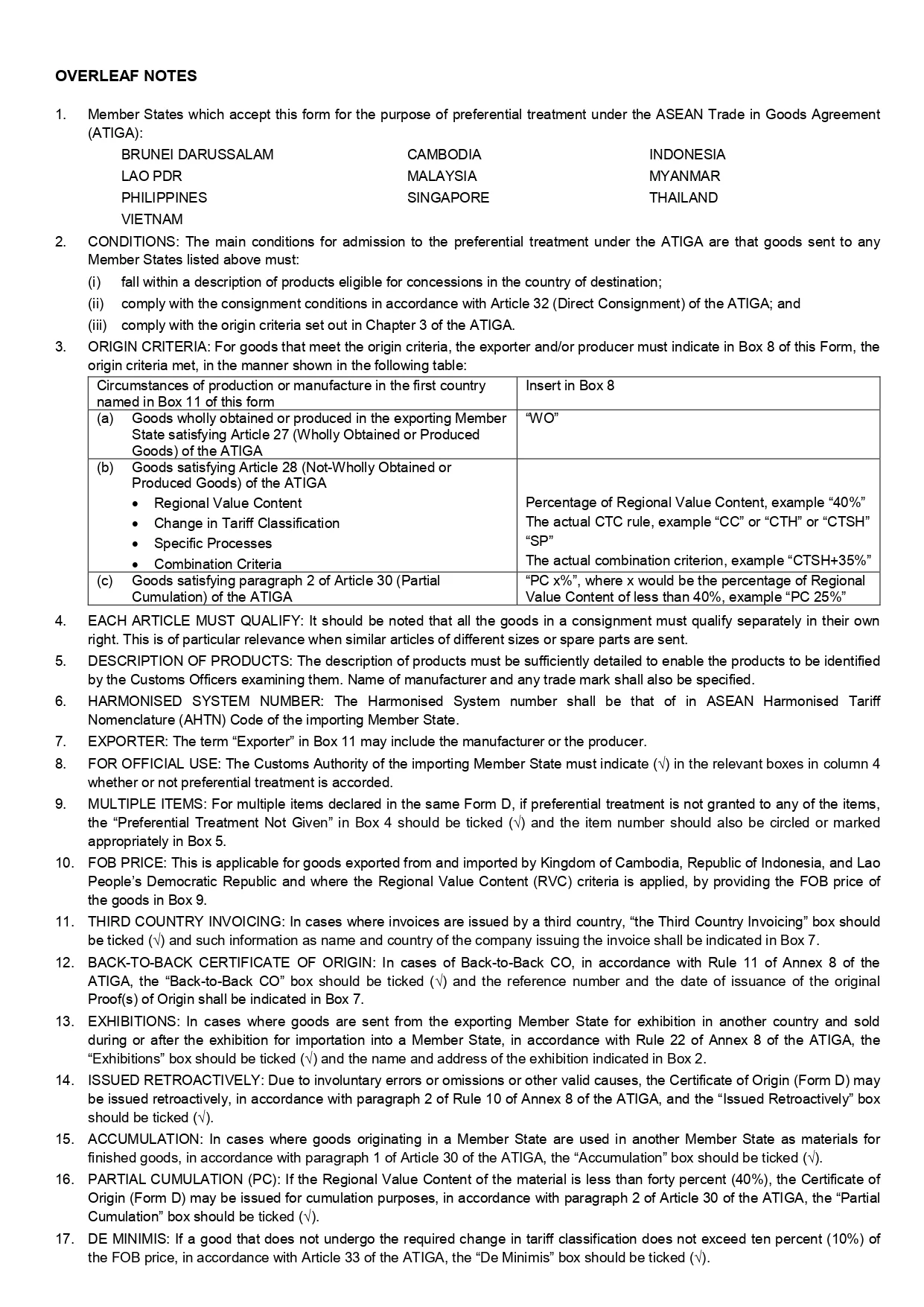

C/O Form D Sample — Page 1

C/O Form D Sample — Page 2

You can also

download the C/O Form D sample here.

The primary purpose of C/O Form D is to allow goods to enjoy ATIGA preferential tariff rates, typically ranging from 0–5%, instead of much higher MFN tariff rates. This creates a direct competitive advantage for import-export businesses within ASEAN.

Read more about C/O Form A here

2. Conditions for obtaining C/O Form D

Origin criteria

To qualify for C/O Form D, goods must satisfy at least one of the following origin criteria:

- WO (Wholly Obtained): Goods are entirely produced in an ASEAN member country without using imported materials from outside ASEAN. Commonly applied to agricultural products, seafood, and natural resources.

- RVC (Regional Value Content of at least 40%): ASEAN-origin materials account for at least 40% of the FOB value of the finished goods. This is the most common criterion for manufactured and industrial products.

- CTC (Change in Tariff Classification): Goods are manufactured using materials classified under different HS codes from the finished product, demonstrating substantial transformation in the exporting country.

Direct consignment rule

Goods must be transported directly from the exporting ASEAN country to the importing ASEAN country without passing through a non-ASEAN country. If goods transit through a third country, businesses must prove that the goods were not altered, commercially traded, or modified during transit and remained under customs supervision.

If these requirements are not satisfied, C/O Form D may lose its preferential tariff validity.

Commercial invoice requirements

The Commercial Invoice used together with C/O Form D must accurately reflect the goods description, cargo value, trade terms, and buyer-seller information.

If a third-country invoice is used, businesses must tick the “Third Country Invoicing” box in Box 13 of C/O Form D and provide details of the invoicing company.

3. Detailed guide to completing C/O Form D

| Box | Field Name | Information Required |

|---|---|---|

| Box 1 | Exporter’s Name, Address and Country | Full name, address, and country of the exporter |

| Box 2 | Consignee’s Name, Address and Country | Full consignee information in the importing country |

| Box 3 | Departure Date / Transport Details | Transport method, vessel or flight details, and departure date |

| Box 4 | For Official Use | Reserved for the issuing authority |

| Box 5 | Item Number | Sequential number of goods items |

| Box 6 | Marks and Numbers on Packages | Marks, labels, and package numbers |

| Box 7 | Description of Goods | Quantity, packaging type, and product description |

| Box 8 | Origin Criterion | Declare WO, RVC, or CTC criteria |

| Box 9 | Gross Weight / FOB Value | Gross weight or quantity; FOB value required for RVC |

| Box 10 | Invoice Number and Date | Commercial invoice number and issuance date |

| Box 11 | Declaration by the Exporter | Exporter’s signature, stamp, place, and date |

| Box 12 | Certification by Competent Authority | Signature and stamp of issuing authority |

| Box 13 | Remarks | Tick applicable boxes such as Issued Retroactively or Third Country Invoicing |

Important notes when declaring C/O Form D

- Box 8 — Origin Criterion: Declare the correct origin rule such as WO, RVC 42%, CTH, or CTSH. Incorrect origin criteria are among the most serious reasons for rejection.

- Box 9 — FOB Value: FOB value is mandatory only when applying the RVC criterion.

- Box 13 — Special remarks:

- Issued Retroactively: Tick if the certificate is issued after exportation.

- Third Country Invoicing: Tick if the invoice is issued by a company located in another country.

- Back-to-Back C/O: Tick when the certificate is issued based on an original ASEAN certificate.

4. C/O Form D application procedure in Vietnam

- Trader registration: First-time exporters must register enterprise information with regional Import-Export Management Offices or VCCI.

- Electronic declaration: Businesses declare shipment information through the EcoSys electronic origin management system at ecosys.gov.vn.

- Online submission and digital signature: Submit the electronic dossier together with a digital signature.

- Receive the approved certificate: After approval, businesses receive the original C/O Form D to send to importers for ATIGA preferential customs clearance.

5. Electronic C/O Form D (e-Form D) and the ASEAN Single Window

e-Form D is the electronic version of C/O Form D, exchanged directly between ASEAN customs authorities through the ASEAN Single Window (ASW).

Instead of sending paper certificates physically, e-Form D is transmitted electronically in real time, helping businesses shorten customs clearance time significantly.

Businesses can verify and track the status of C/O Form D through the official EcoSys portal or Vietnam’s VNACCS/VCIS electronic customs system.

Benefits of e-Form D include:

- Reducing document fraud risks

- Faster customs clearance

- Lower storage and administrative costs

- Reduced paperwork for import-export businesses

6. Common mistakes causing C/O Form D rejection

- Incorrect HS code: HS codes on the certificate do not match customs declarations or importing country classifications.

- Mismatch between C/O, Invoice, and B/L: Product names, quantities, values, or consignee information are inconsistent.

- Signature and stamp issues: Unauthorized signatures or unclear company seals.

- Expired certificate: C/O Form D is valid for only 12 months from issuance.

- Failure to tick “Issued Retroactively”: Missing this declaration may lead customs authorities to reject the certificate.

- Incorrect origin criteria in Box 8: Declaring incorrect RVC or CTC criteria can result in tax reassessment and penalties.

FAQ — Frequently Asked Questions about C/O Form D

How long is C/O Form D valid?

C/O Form D remains valid for 12 months from the issuance date.

Can C/O Form D be used for Chinese goods?

No. C/O Form D applies only to ASEAN-origin goods traded within ASEAN. Goods originating from China require C/O Form E under the ASEAN-China Free Trade Agreement (ACFTA).

What should businesses do if there is incorrect information on C/O Form D?

Businesses must contact the issuing authority immediately to cancel the incorrect certificate and request a replacement. Altering the original certificate manually is prohibited and may be considered document fraud.

Conclusion

C/O Form D is an essential legal document helping businesses reduce import duties in ASEAN trade, with tariff rates potentially reduced to 0% under ATIGA.

However, to avoid rejection and loss of tariff benefits, businesses should carefully review all information before submission, including HS codes, origin criteria, consistency between shipping documents, and special remarks in Box 13.

Investing time in preparing accurate documentation from the beginning can help businesses avoid customs disputes, tax reassessments, administrative penalties, and damage to international trade relationships.

CONTACT INFORMATION

3W Logistics — Ho Chi Minh City Headquarters

Address: 34 Bach Dang Street, Tan Son Hoa Ward, Ho Chi Minh City, Vietnam

Hotline: +84 28 3535 0087

3W Logistics — Hai Phong Branch

Address: 8A Lot 28 Le Hong Phong Street, Gia Vien Ward, Hai Phong City, Vietnam

Hotline: +84 225 355 5939

3W Logistics — Hanoi Branch

Address: 81A Tran Quoc Toan Street, Cua Nam Ward, Hanoi, Vietnam

Hotline: +84 24 3202 0482

3W LOGISTICS CO., LTD — We here serve you there!

Email:quote@3w-logistics.com

Website: www.3w-logistics.com

Facebook: 3W Logistics Co., Ltd